See also

Film about the BCL's missions and tasks

The Banque centrale du Luxembourg (BCL) informs that, based on preliminary data, the main interest rates applied by Luxembourg’s credit institutions to euro area households and non-financial corporations (NFCs) for their loan and deposit operations have on average evolved as follows in December 2025.

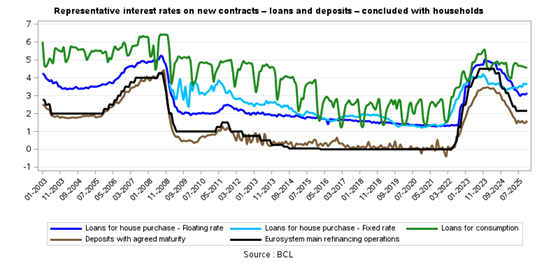

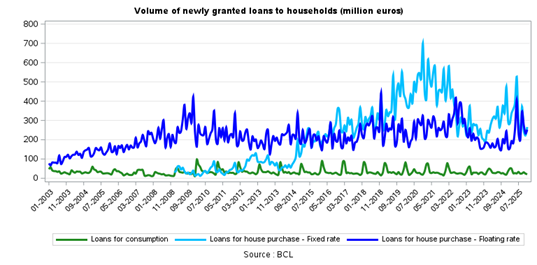

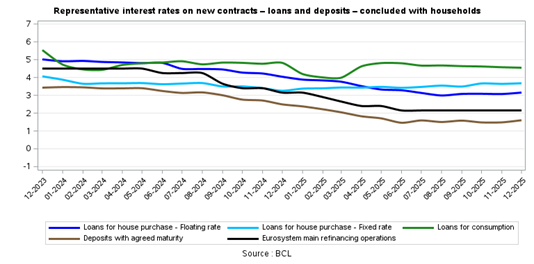

Representative interest rates on new contracts[1] – loans and deposits – concluded with households

The variable[2] interest rate on mortgage loans granted to households has increased by 8 basis points on a monthly basis to reach 3.15% in December 2025 compared to 3.07% in November 2025 and the volume of these newly granted loans has increased by 20 million euros to reach 252 million euros in December compared to 232 million euros in November. On a yearly basis, the interest rate has decreased by 89 basis points whereas the volume of newly granted loans has increased by 7 million euros.

The fixed[3] interest rate on mortgage loans granted to households with an initial fixation rate of over one year and up to five years increased by 3 basis points on a monthly basis to reach 3.30% in December 2025 while the volume reaches 31 million euros. The fixed interest rate with an initial fixation rate of over five years and up to ten years increased by 13 basis points compared to November 2025 to reach 3.68%. The corresponding monthly volumes increased by 5 million euros to reach 54 million euros.

Concerning real estate loans with an initial rate fixation period over 10 years, the monthly volumes increased by 36 million euros since November to reach 181 million euros. Interest rates of these loans are grouped by intervals of five years of initial rate fixation[4], and have changed as follows compared with November 2025:

It is important to mention that the indicated rates of the different interest rate fixations are average rates, where the calculations are based on a sample of banks and which are taking into account the volumes of granted loans.

The interest rate on consumer loans that have an initial fixation period above 1 year and below or equal to 5 years has decreased by 3 basis points since November to reach 4.55% in December 2025. The volume of newly granted loans has decreased by 3 million euros to reach 21 million euros in December compared to 24 million euros in November. On a yearly basis, the interest rate has decreased by 27 basis points whereas the volume of new lending has increased by 2 million euros.

The interest rate on households’ fixed-term deposits that have an initial maturity below or equal to 1 year has reached 160 basis points in December 2025 from 148 basis points in November 2025. On a yearly basis, this rate has decreased by 89 basis points.

The following graphs provide a detailed overview of the evolution of interest rates and the volumes of the new business loans. Furthermore, the evolution of the interest rates over the past two years is presented in more detail.

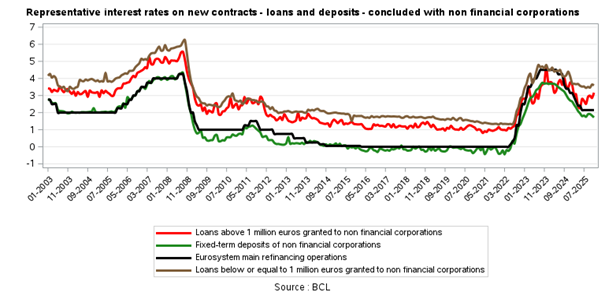

Representative interest rates on new contracts1 – loans and deposits – concluded with non-financial corporations (NFCs)

The variable interest rate on loans below or equal to 1 million euros granted to NFCs decreased by 5 basis points in December 2025 to 3.59%, compared to 3.64% in November, and the volume has decreased by 2 million euros to reach 119 million euros in December from 121 million euros in November. On a yearly basis, this interest rate has decreased by 54 basis points and the volume of newly granted loans has increased by 16 million euros.

The variable interest rate on loans above 1 million euros granted to NFCs has increased by 31 basis points on a monthly basis to 3.17% during the last reference period, compared to 2.86% in November. The volume of newly granted loans has increased by 971 million euros to reach 2 869 million euros in December compared to 1 898 million euros in November. On a yearly basis, this interest rate has decreased by 59 basis points and the volume of newly granted loans has increased by 942 million euros.

The interest rate on fixed-term deposits of NFCs with an initial maturity below or equal to 1 year decreased by 10 basis points on a monthly basis since November to reach 1.72% in December 2025. On a yearly basis, this interest rate has decreased by 99 basis points.

The tables pertaining to interest rates applied to credit institutions can be consulted and/or downloaded on the BCL’s website on the following link:

https://www.bcl.lu/en/statistics/series_statistiques_luxembourg/03_Capital_markets/index.html

Weighting method

The interest rates applied to new contracts are weighted within the categories of instruments concerned by the amounts of individual contracts. This results from the compilation of national aggregates carried out by reporting credit institutions and by the BCL.

[1] New contracts refer to any new agreement concluded between the household or the non-financial corporation and the reporting agent. New contracts include all financial contracts which mention for the first time the interest rate pertaining to the deposit or credit and all renegotiations of existing deposits or credits.

[2] Variable interest rate or rate with an initial fixation period inferior or equal to 1 year.

[3] Fixed interest rate weighted by the amounts of contracts for all mortgage loans granted, whatever the initial rate fixation period (above 1 year). This series has been published by the BCL since February 2009 only for methodological reasons linked to the identification of reporting agents.

[4] Following an update of the statistical data collection, since December 2022 the BCL has been collecting a breakdown of interest rates with an initial fixation rate of over 10 years in five-year intervals.