Useful links

- European Central Bank publications

25/03/2022

Blog post by Gaston Reinesch, Governor of the BCL

THE MARCH 2022 ECB GOVERNING COUNCIL MONETARY POLICY DECISIONS: REASSESSING THE INFLATION OUTLOOK AND RECALIBRATING MONETARY POLICY NORMALISATION [1]

In December 2021 the Governing Council assessed that the progress on economic recovery and towards its medium-term inflation target permitted a step-by-step reduction in the pace of its asset purchases.

Back then, the Governing Council had decided to discontinue net asset purchases under the Pandemic Emergency Purchase Programme (PEPP) at the end of March 2022.

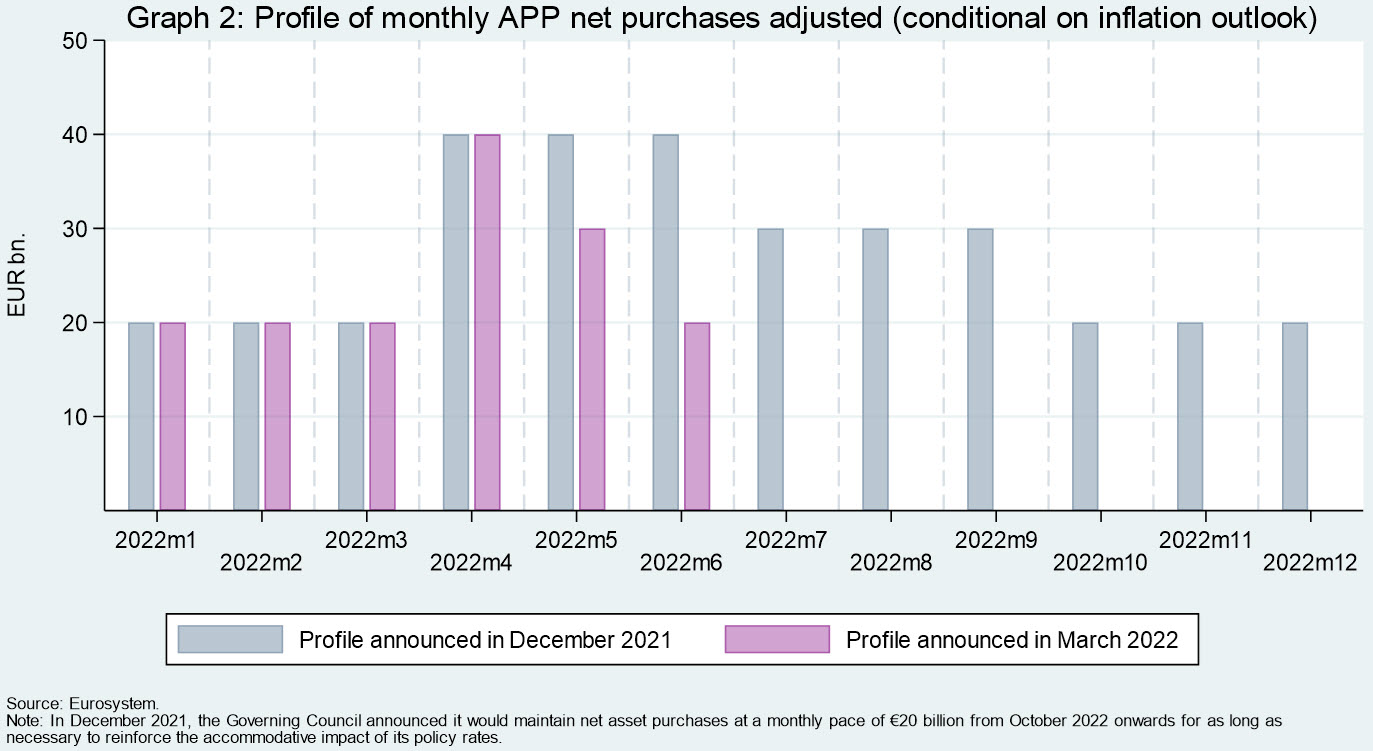

The Governing Council also announced that the monthly net purchases under the Asset Purchase Programme (APP) would amount to €40 billion in the second quarter of 2022 and to €30 billion in the third quarter. From October 2022 onwards, the Governing Council would maintain net asset purchases under the APP at a monthly pace of €20 billion for as long as necessary to reinforce the accommodative impact of its policy rates.

On 3 February 2022, the Governing Council confirmed the step-by-step reduction in asset purchases and recalibrated its monetary policy statement, acknowledging that Inflation had further surprised to the upside in January 2022 and pointing out that “compared with our expectations in December, risks to the inflation outlook are tilted to the upside, particularly in the near term”.[2]

At its meeting on 10 March 2022, in the context of the war in Ukraine and the March 2022 ECB staff macroeconomic projections, the Governing Council reassessed the euro area inflation outlook.

Prior to the Russia-Ukraine war, the underlying conditions for the euro area economy were solid, reflecting ample policy support, improving labour markets, the fading impact of the Omicron coronavirus variant and first signs of easing supply bottlenecks. At the same time, inflation continued to surprise on the upside.

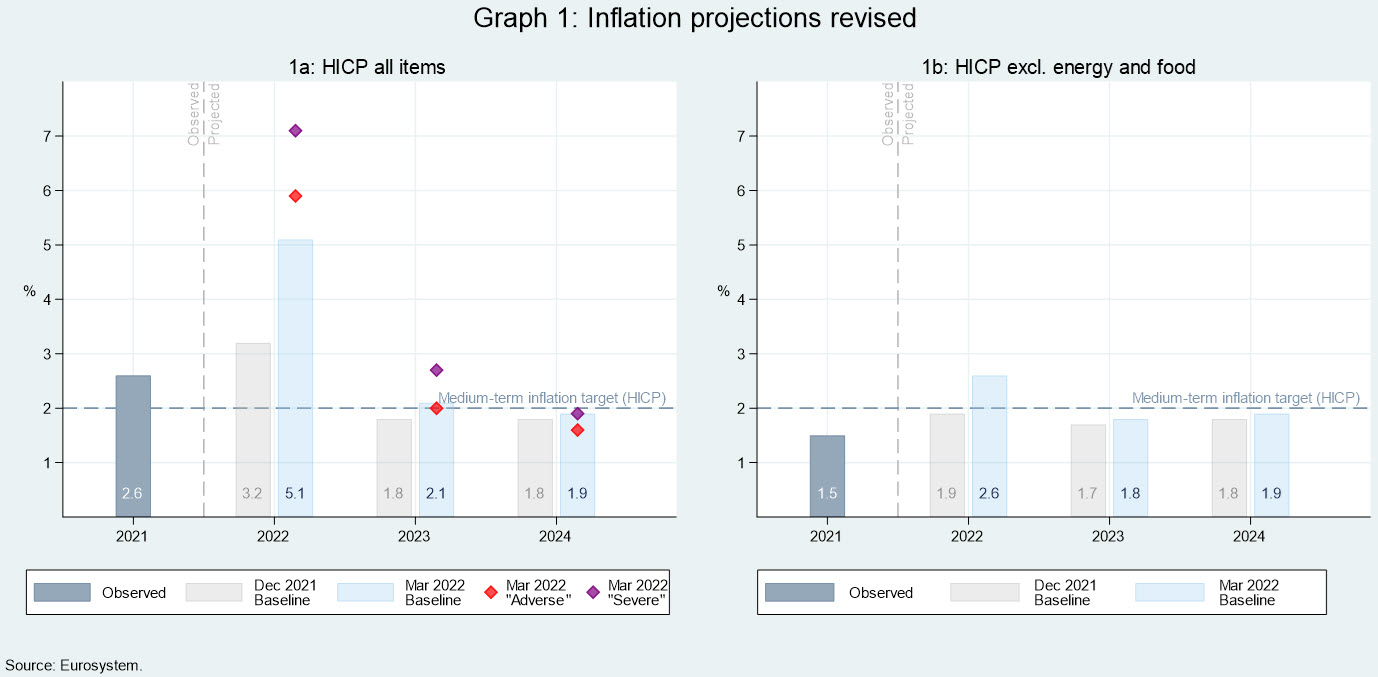

While hardly possible to assess in all its horror, the war in Ukraine’s impact on economic activity and inflation through higher energy and commodity prices, the disruption of trade and weaker confidence is material and accordingly, the March 2022 staff projections point to lower GDP growth compared with the December 2021 projections whereas the baseline for inflation projections has been revised significantly upwards, with annual inflation at 5.1 per cent in 2022, 2.1 per cent in 2023 and 1.9 per cent in 2024 (up from 3.2, 1.8 and 1.8 per cent, respectively according to the December 2021 projections, see Graph 1a below).

In recognition of the very elevated uncertainty, in early March, the Governing Council considered - next to the baseline scenario - two alternative scenarios (dubbed “adverse scenario” and “severe scenario”). Both scenarios suggest an even higher inflation rate for this year. The “severe” scenario projects higher inflation also in 2023.

Needless to say, the various scenarios can only provide a tentative and incomplete assessment of the implications of the possible economic impacts of the war in Ukraine.[3]

As far as price pressures are concerned, while largely limited to HICP energy items initially, they have become more broad-based over recent months. Accordingly, various measures of underlying inflation have increased to levels above two per cent. Thus, the baseline scenario suggests an inflation rate excluding food and energy items of 2.6 per cent in 2022, 1.8 per cent in 2023 and 1.9 per cent in 2024, again higher than in the December 2021 projections (see Graph 1b above).

Based on the updated assessment of the inflation outlook and taking into account the very elevated uncertainty, for now, the Governing Council all by all sees it as increasingly likely that inflation will stabilise at its two per cent target over the medium term. If price pressures feed through into higher than anticipated wage rises or if there will be additional adverse persistent supply-side implications, inflation could even turn out to be higher over the medium term. However, if demand were to weaken over the medium term, this could also lower pressures on prices.

Based on its updated assessment of the inflation outlook and in line with the February 2022 monetary policy statement, the Governing Council in March revised significantly the purchase schedule for the APP for the coming months.[4]

Monthly net purchases under the APP will amount to €40 billion in April, €30 billion in May and €20 billion in June (see Graph 2 below).

Not only did the Governing Council renounce to give, as in December 2021, any quantitative indication of net purchases in the third quarter and beyond, but moreover it considered that if incoming data would continue to support the expectation that the medium-term inflation outlook will not weaken, net asset purchases under the APP could be concluded already in the third quarter. In the latter scenario, the actual end date/month (i.e. July, August or September) would depend on the Governing Council’s assessment of the inflation outlook over the coming months.

Given the high uncertainty, the Governing Council did however not omit to stress that it stands ready to revise the schedule for net asset purchases in terms of size and/or duration.

Without prejudice to the uncertainties due to the war in Ukraine and without prejudice to and conditional on the Governing Council’s assessment of the inflation outlook in the coming months, a possible end of net asset purchases in 2022Q3 - provided the inflation outlook is corroborated - marks an important change from the more “open” (yet also conditional) communication about the APP net purchase horizon in place since September 2019.[5]

As a next step in a gradual and data-dependent normalisation process[6], an end to net asset purchases under the APP would mean that net asset purchases fulfilled their objective to reinforce the accommodative impact of the policy rates[7], in line also with the principle of proportionality. This process follows a period of several years characterised by a very accommodative monetary policy (including, among others, a negative deposit facility interest rate, large-scale asset purchases and longer-term refinancing operations).

Its intention to reinvest, in full, the principal payments from maturing securities until at least the end of 2024 (PEPP)[8] and for an extended period of time past the date when the Governing Council starts raising key interest rates (APP)[9] continues to imply substantial monetary accommodation through the stock of assets held by the Eurosystem (approximately € 4.9 tn in mid-March 2022).

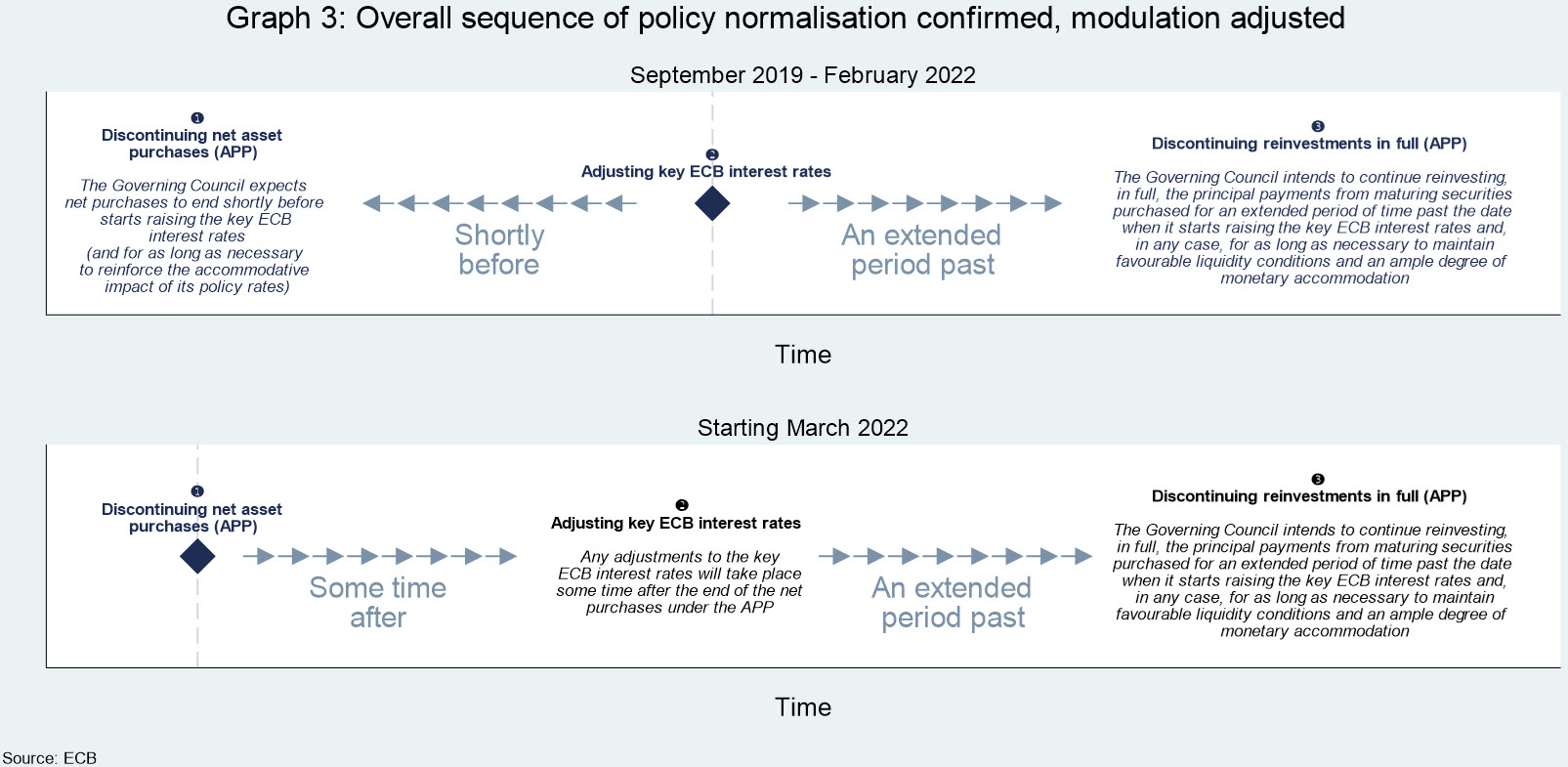

While in March 2022 the Governing Council confirmed the overall chronological sequence of policy normalisation laid out in September 2019[10], it adjusted its communication on the modulation of the end of net APP purchases and an adjustment to the key ECB policy rates.[11]

Between September 2019 and February 2022, both the expected end of net purchases under the APP (“shortly before the Governing Council starts raising the key ECB interest rates”) and the intended duration of reinvestments (“an extended period of time past the date when the Governing Council starts raising the key interest rates”) were “chained” to the timing of the rate lift-off (see upper panel in Graph 3 below).

In March 2022, the Governing recalibrated the “chained” sequence. It complemented the new (conditional) end date for net APP asset purchases by announcing that any gradual and data-dependent adjustments to the key ECB interest rates would take place “some time after” the end of net asset purchases (see lower panel in Graph 3 above).

The expression “some time” provides the Governing Council, in the current circumstances characterised by Knightian uncertainty[12], with a much needed flexibility/optionality as to the length of the period between an end of net asset purchases and a first rate hike.

At the same time, it may not be misperceived as suggesting the period between an end to net purchases and a rate hike would be rather long or subject to discretion. Depending on the state of the economy and the inflation outlook, the term “some time” might characterise a period as short as a couple of weeks or, alternatively, stretching over some months.

The timing of a first rate hike will continue to be data-dependent, determined by the Governing Council’s forward guidance and by its strategic commitment to stabilise inflation at 2% over the medium term.[13]

Contingent on the war in Ukraine triggering no additional disruptive economic and financial impacts, it would therefore not be entirely groundless, based on the March Governing Council monetary policy decisions, to consider a first rate hike in the second half of 2022.

[1] I would like to thank Patrick Lünnemann for support in preparing this article.

[2] See our blog article « The February 2022 Governing Council: Monetary policy decisions confirmed, monetary policy statement recalibrated”).

[3] The scenarios are not meant to capture in full the impact of genuine tail events.

[4] In March the Governing Council also adjusted its communication on the key ECB interest rates going forward. First, the forward guidance on the key ECB interest rates in the March 2022 monetary policy decisions refers to the Governing Council expecting the key ECB interest rates to remain at their present levels (previously present or lower levels). Second, the March 2022 monetary policy decisions no longer state that the period over which the Governing Council expects the key ECB interest rates to remain unchanged may also imply a transitory period in which inflation is moderately above target.

[5] In September 2019, the Governing Council decided to restart net asset purchases under the APP at a monthly pace of €20 billion, expecting them to run for as long as necessary to reinforce the accommodative impact of its policy rates, and to end shortly before it started raising the key ECB interest rates.

[6] Given the progress on economic recovery and towards its medium-term inflation target, in December 2021 the Governing Council had already decided to discontinue net purchases under the PEPP in March.

[7] In December 2021 the Governing Council announced it would maintain net asset purchases (at a monthly pace of € 20 billion) for as long as necessary to reinforce the accommodative impact of its policy rates.

[8] In any case, the future roll-off of the PEPP portfolio will be managed to avoid interference with the appropriate monetary policy stance.

[9] And, in any case, for as long as necessary to maintain favourable liquidity conditions and an ample degree of monetary accommodation.

[10] Namely to first end net APP purchases, then to adjust key interest rates and, subsequently, to end reinvestments of the principal payments from maturing securities purchased.

[11] On 24 March 2022, the Governing Council also announced it will gradually phase out the pandemic collateral easing measures introduced in April 2020. The step-wise phasing out of measures between July 2022 and March 2024 will gradually restore the Eurosystem’s pre-pandemic risk tolerance and avoid collateral availability cliff effects (ECB press release of 24 March 2022).

[12] Including known unknowns and unknown unknowns.

[13] Accordingly, at present, the Governing Council expects the key ECB interest rates to remain at their present levels until it sees inflation reaching 2% well ahead of the end of its projection horizon and durably for the rest of the projection horizon, and it judges that realised progress in underlying inflation is sufficiently advanced to be consistent with inflation stabilising at 2% over the medium term.