Lien utile

- Publications de la Banque centrale européenne

Blog post by Gaston Reinesch, Governor of the BCL

The blog post “28/ Money Market Statistical Reporting (MMSR): Enlarged reporting population including three reporting agents based in Luxembourg” highlighted the essential role of high‑quality statistical information for understanding euro area money markets and emphasised, in particular, the centrality of the Money Market Statistical Reporting (MMSR) framework. Since its inception, the MMSR has provided the Eurosystem with a uniquely granular and timely view of money market activity, offering a level of granularity, frequency and standardisation that had previously been unattainable. A high‑frequency and transaction‑level view of money market conditions is essential for assessing the transmission of monetary policy, as these markets are the first to reflect changes in policy rates and liquidity conditions. The MMSR therefore enables the Eurosystem to monitor how policy impulses propagate across segments, maturities and counterparties on a day-to-day basis.

For many years, public access to MMSR‑based insights rested on two principal dissemination channels.

In recent years, the ECB has increasingly drawn on MMSR evidence across a wide range of other communication outlets. Examples include speeches and commentaries on, inter alia, changes to the ECB’s operational framework[3], assessments of money market funding[4] and discussions of repo market conditions[5]. MMSR‑based insights have thus become a recurring reference point in the ECB’s communication, reflecting the dataset’s relevance for policy analysis.

The academic community likewise recognised the analytical value of MMSR data. A growing body of research now uses MMSR-based data to study, for example, the transmission of interest rate hikes to money market repo rates[6], collateral scarcity and repo market conditions[7], determinants in the supply of dollar funding[8], or variations in the repo-deposit facility spread in the euro area[9]. The MMSR has thus become a cornerstone of empirical money market research, enabling analyses that were simply not feasible with earlier survey‑based or aggregate data sources.

By late April 2026, the ECB has substantially enhanced both the accessibility and the presentation of its money market statistics, making the data offering more intuitive, more comprehensive and even more user‑friendly. At the centre of this effort stand two major innovations.

First, the Extended Money Market Statistics (EMMS) Dataset, now integrated into the ECB’s Data Portal, adds a further 352 time series, thereby significantly enriching the MMSR‑based statistical offering.

Second, the launch of the Extended Money Market Statistics (EMMS) Dashboard provides immediate access to MMSR‑information. The dashboard curates, structures and visualises the newly available EMMS series into a coherent and analytical interface.

The dashboard covers the four MMSR segments - secured, unsecured, OIS and FX swaps – as well as the short‑term securities segment for a more comprehensive view of short‑term funding markets. The interactive nature of the dashboard allows users to access money market information intuitively. Beyond this, the new dashboard enables users to explore developments across the money market in multiple dimensions and breakdowns - including volumes, prices, counterparties, maturities and calendar effects - thereby offering a far richer view of market behaviour than previously available. As a result, the dashboard is not merely a digital companion to the €MMS but a comprehensive analytical tool that strengthens the ECB’s statistical communication and supports both policy analysis and academic research. The published time series generally span the period from early 2017 to the end of 2025, with updates released once a year.

The Overview section of the EMMS Dashboard is designed as a concise gateway into the structure and dynamics of the euro money market. It presents four headline charts. Chart 1a and Chart 1b will be briefly discussed by way of example.

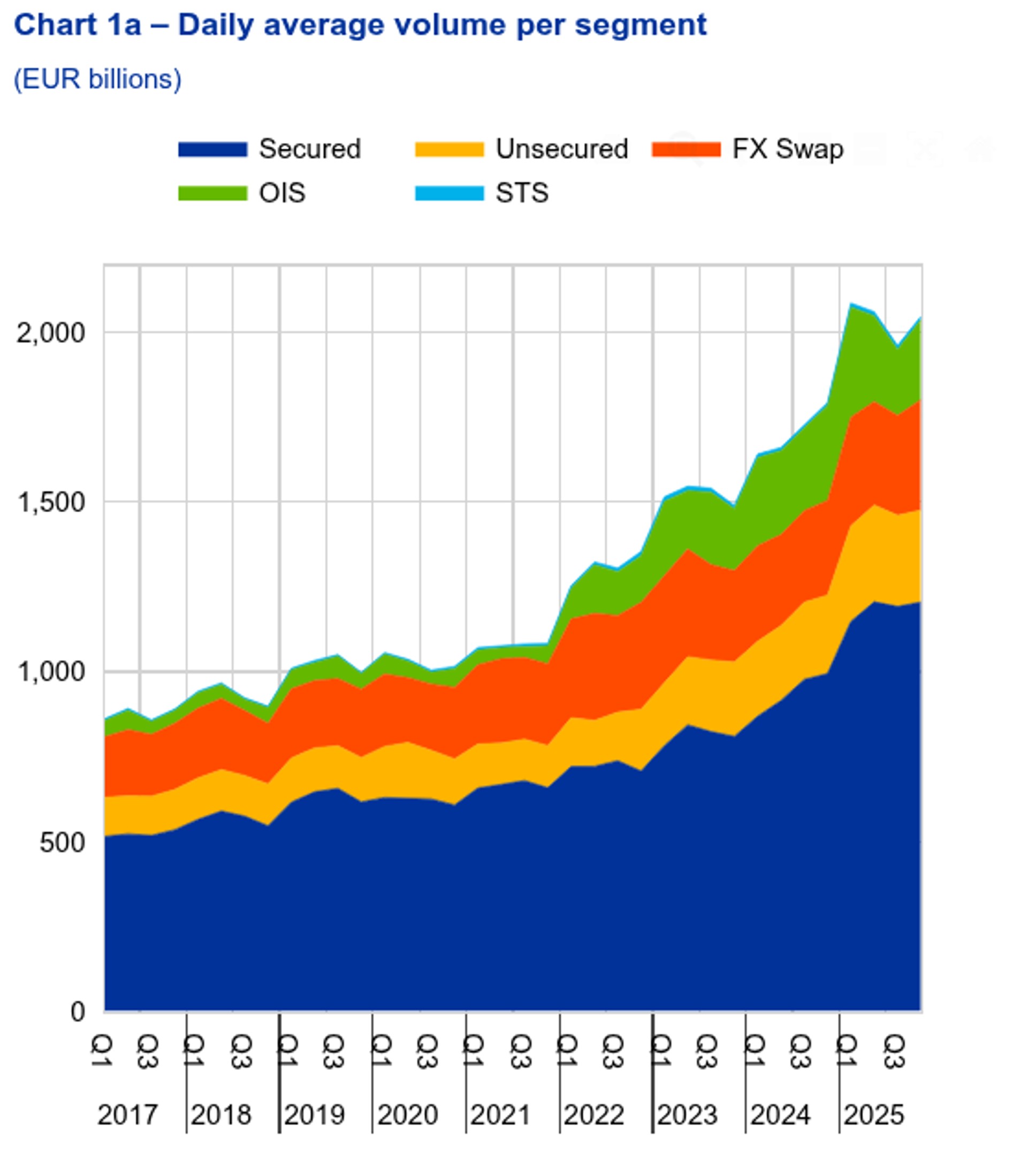

Chart 1a illustrates the daily average volume of transactions for each of the five money market segments.

By 2025-Q4, secured transactions remained by far the largest segment, with average trading volumes rising to 1,205.2 billion Euro from 994.7 billion Euro a year earlier, followed by the FX swap segment, where average volumes increased to 325.6 billion Euro (2024‑Q4: 279.1 billion Euro). Activity in the unsecured market also expanded, reaching 270.7 billion Euro compared with 231.1 billion Euro in late 2024. By contrast, OIS turnover declined to 235.1 billion Euro from 279.2 billion Euro, while the short‑term debt securities segment remained comparatively small, edging up to 10.1 billion Euro from 9 billion Euro (y-o-y).

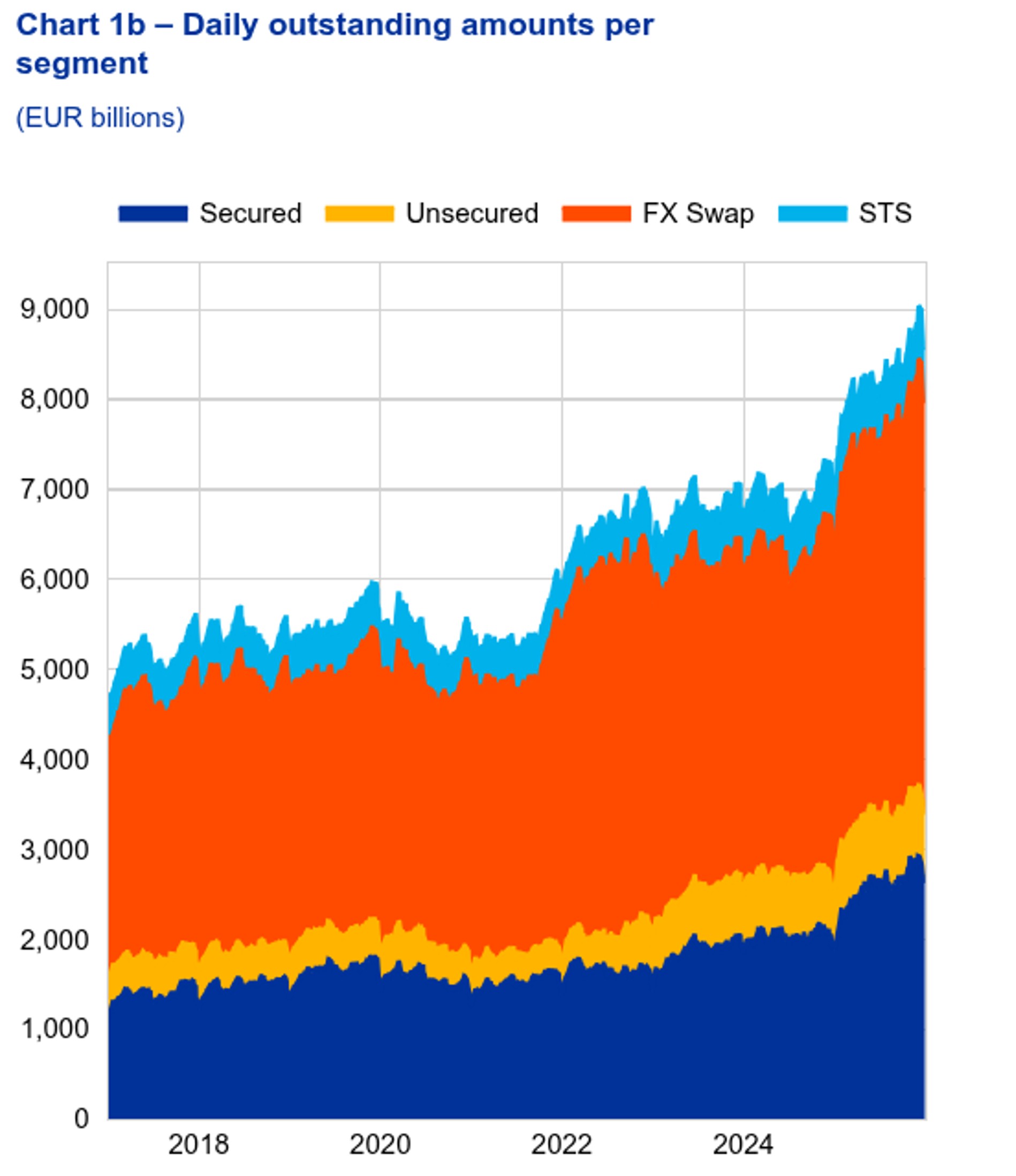

Chart 1b, on the other hand, takes a closer look at the outstanding amounts by money market segment.[10]

FX swaps represent by far the largest share of outstanding amounts, with positions rising to 4,590 billion Euro as at 31 December 2025, up from 3,861 billion Euro a year earlier. Secured instruments form the second‑largest segment, increasing to 2,623 billion Euro compared with 1,870 billion Euro at the end of 2024. Outstanding amounts in the unsecured market also expanded, reaching 761 billion Euro (31 December 2024: 657 billion Euro), while the short‑term debt securities segment remained broadly stable at 590 billion Euro, only slightly below its 593 billion Euro level a year earlier.

A comparison of the two charts shows that secured transactions dominate daily volumes because repos are short‑term and are rolled over continuously, generating high turnover but relatively small outstanding amounts. FX swaps show the opposite pattern: they are traded less frequently, yet their longer maturities accumulate into large outstanding amounts.

The remainder of the EMMS Dashboard provides comprehensive information on “Volumes”, “Rates”, “Counterparties” and “Maturities” for each of the five segments of the money market.

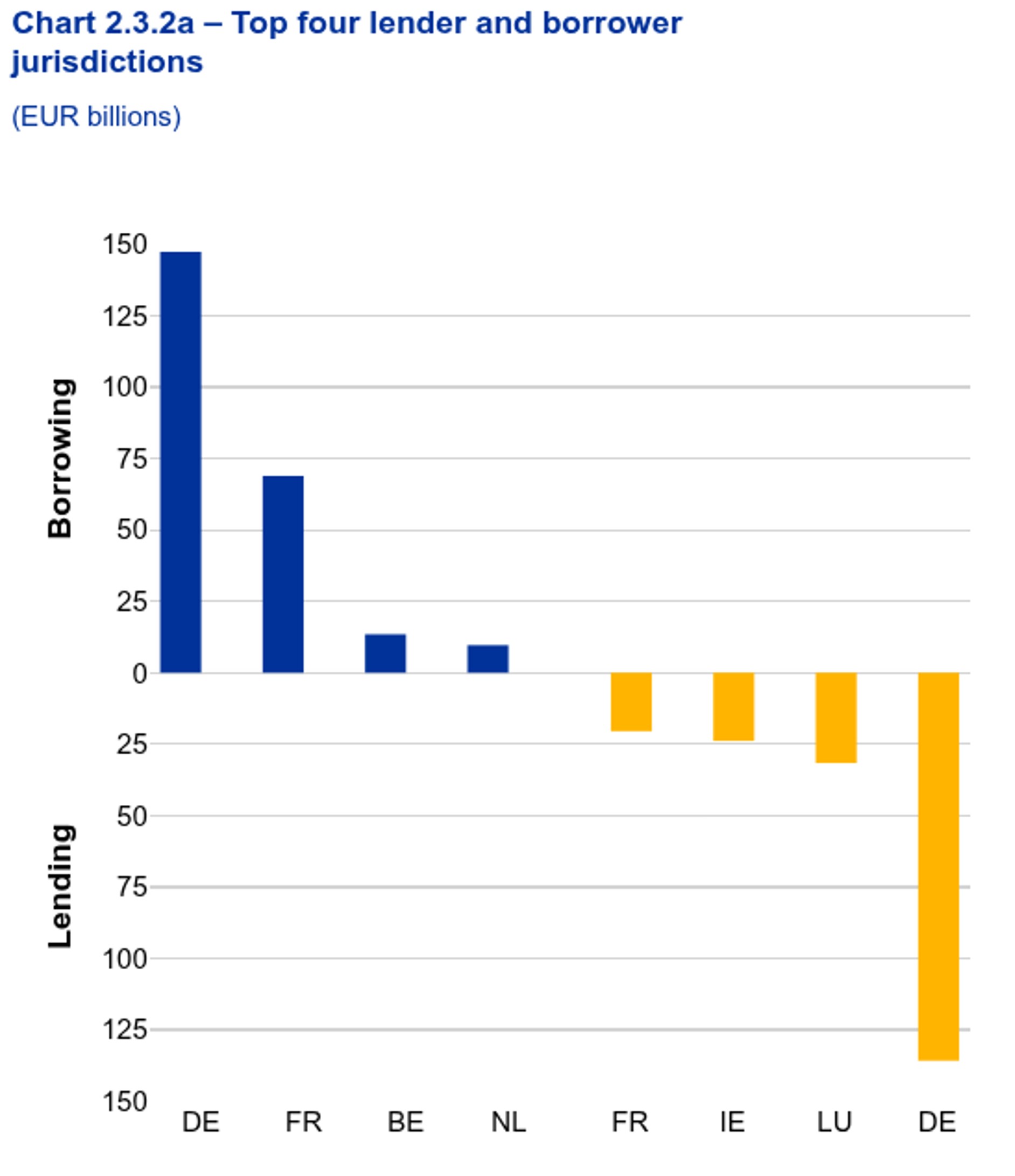

Among others, the EMMS Dashboard confirms the role of Luxembourg for the euro money market. As regards the unsecured segment (Chart 2.3.2a), Luxembourg ranks second-largest amongst the top four lending jurisdictions with around 31.7 billion Euro in lending volumes in 2025.

Luxembourg’s prominent position in the unsecured segment stems from the presence of several internationally active banks operating from the Grand Duchy. These institutions use Luxembourg as a platform for cross-border treasury operations and liquidity management.

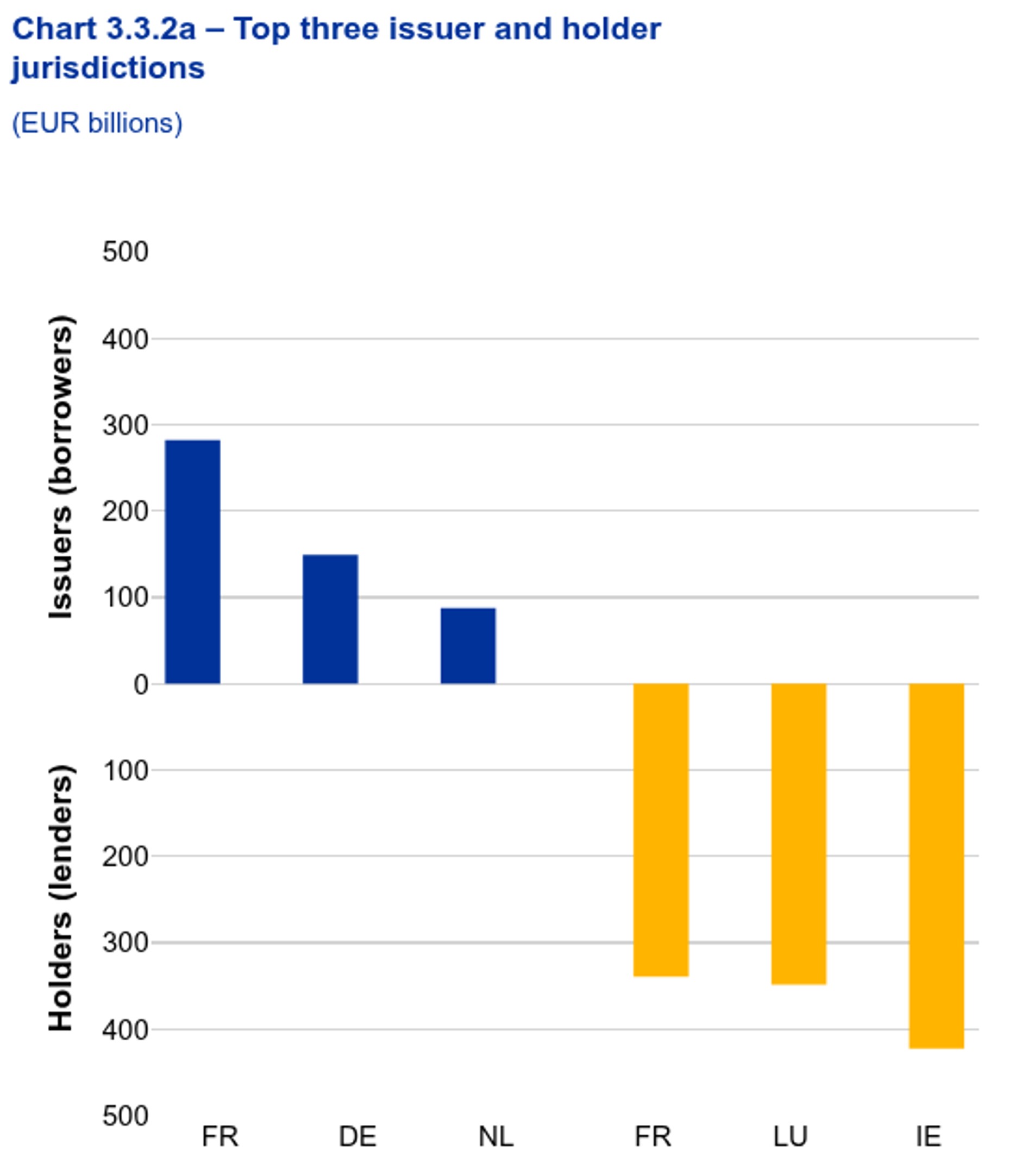

As part of the short-term securities segment (Chart 3.3.2a), Luxembourg ranks second amongst the top holders with a volume of approximately 348.8 billion Euro recorded for 2025.

This reflects Luxembourg’s role as a major European centre for investment funds and securities custody, where substantial cross‑border portfolios are administered.

______________________________________________________

[1] I would like to thank Martin Lempe and Christophe Kieffer for their support in preparing this article.

[2] Beyond the data series, the portal also offers essential contextual material under “Data information” and “Data structure” to guide users through the methodological underpinnings of the dataset. These explanatory notes are indispensable for analysts seeking to interpret MMSR data correctly, particularly given the complexity of transaction‑level reporting and the variety of instruments across segments. Although the “MMSR Dataset” contains 446 time series in total, the eight “Pre-Euro Short-Term Rate” series are excluded from this count.

[3] Cf. The ECB Blog (2025), The first year of the Eurosystem’s new operational framework, 25 April 2026 [https://www.ecb.europa.eu/press/blog/date/2025/html/ecb.blog20250425~fa1fb8e9ac.en.html].

[4] Cf. The ECB Blog (2026), How banks are adjusting to declining reserves, 2 April 2026 [https://www.ecb.europa.eu/press/blog/date/2026/html/ecb.blog20260402~d9be74e490.en.html].

[5] Cf. Schnabel (2025), Towards a new Eurosystem balance sheet, Speech at the Chicago Booth Conference on the Global Economy and Financial Stability, London, 15 November 2025 [https://www.ecb.europa.eu/press/key/date/2025/html/ecb.sp251115~cf1d96a0e4.en.pdf].

[6] Cf. Nguyen et al. (2023), Safe Asset Scarcity and Monetary Policy Transmission, Working paper 934, Banque de France.

[7] Cf. Greppmair et al. (2025), Collateral Easing and Safe Asset Scarcity: How Money Markets Benefit from Low-Quality Collateral, Bundesbank Discussion Paper 20/2025.

[8] Cf. Du et al. (2025), Repo and FX Swaps : A Tale of Two Markets, Harvard Business School, Working paper.

[9] Cf. Vela, Aguilar (2024), The Impact of Monetary Policy Normalisation on Secured Money Markets, Banco de España Economic Bulletin 04-2024.

[10] To ensure conceptual clarity, the OIS segment is not included here, as it differs in nature from the other money‑market instruments. OIS transactions refer to a notional amount that is not settled, which distinguishes them from the remaining (non‑OIS) segments where actual monetary transfers are executed.